Daily news feeds carry information about economic data, political developments and other news items. This information can affect asset prices. The challenge facing investors and market analysts is to digest this information and make investment decisions.

Collaborative research between Rice University statistics and finance professors Katherine Ensor and Barbara Ostdiek, statistics doctoral alumnus Yu Han, and Stuart Turnbull, a finance professor at the University of Houston and risk management consultant, investigated the impact news sentiment has on crude oil futures.

In a paper, published in the June 26 issue of the Journal of Asset Management, the researchers introduced a new description of asset pricing dynamics that considers different types of news information in its measurements. Results showed that the effects of negative and positive news can be described by different processes.

“We found a significant proportion of volatility is explained by news arrival, and that negative news has a higher negative impact on returns and volatility clustering than positive news,” said Ensor, the Noah G. Harding Professor of Statistics and director of the Center for Computational Finance and Economic Systems (CoFES).

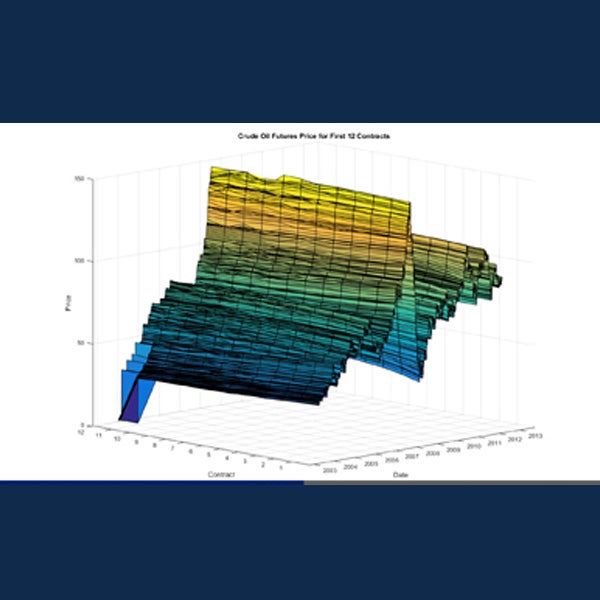

To conduct their research the team built a stochastic model for the analysis of time-series data from Treasury bill interest rate data and oil derivative markets traded on the Chicago Mercantile Exchange from January 2004 to the end of December 2012. They then investigated the impact that information had on news sentiment.

“We chose the discrete-time modeling technique for its ability to analyze the order and timing of multiple events. In any period, a random number of news items might arrive, such as a production announcement from OPEC to daily Brent oil price reports. Each type of news item will have a different impact on prices and hence volatility,” said Turnbull, who is a professor emeritus at the University of Houston’s Bauer College of Business. He specializes in the valuation and modeling of complex securities.

To measure the impact of information flow, the team used word analysis and machine learning technologies. They collected and correlated large data banks of different types of news articles taken from the Thomson Reuters News Analytics (TRNA), which is a natural language processing system that collects, reads, and scores Reuters news articles in real time.

“Machine learning makes it possible to extract useful information from major and normal information events, analyze market linkages and jump intensities, and form the most accurate predictions possible that affect oil prices,” said Ensor.

“Although news articles varied over time, some news is anticipated, like scheduled job market reports or the Energy Information Agency petroleum storage report,” added Ostdiek. “So we further divided major news into two separate groups: major negative news, which correlated with futures price decreases, and major positive news, which correlated with futures price increases.”

Ostdiek is the senior associate dean of degree programs and associate professor of finance at Rice’s Jones Graduate School of Business.

Han says there have been many studies that investigate the impact of news on futures markets as an endogenous process. “This paper shows how language processing technologies can be combined with quantitative strategies to measure the impact that outside unexpected, or exogenous, factors have on futures markets. The model can be applied to address quantitative finance strategies across markets, asset classes, and trading frequencies to assess risk and support decision making.”

Han, who earned his Ph.D. in statistics in 2016 with Ensor serving as his adviser, also worked on a volatility modeling project with Ostdiek through CoFES.

Now a senior data scientist at a startup health insurance company called Oscar Health, Han is using off-the-shelf technologies, such as machine learning, to differentiate the firm from traditional insurance providers.

Since its founding in 2002, CoFES researchers have specialized in modeling dynamic microeconomic and macroeconomic systems, econometrics, and in the development of algorithms and forecasting techniques based on high-dimensional time-series data, artificial intelligence and machine learning, blockchain technologies, Bayesian methods, and stochastic processes.

Knowledge gained through CoFES research is disseminated through undergraduate and graduate curriculum, publications and technical reports, Eubank Conferences and short courses, as well as through leadership and involvement in professional associations.

- Shawn Hutchins, Communications and Marketing Specialist